FREE Uber Tax Info Pack

FREE 5-Day Email Course to learn the ATO’s Uber tax rules

FREE Uber Expense Spreadsheet so you never miss a deduction

FREE Uber Logbook Spreadsheet to claim your car expenses

FREE ABN & GST Registration (if you need it!)

FREE Uber Tax Info Pack

> FREE 5-Day ‘Uber Tax Essentials’ eCourse

> FREE Uber Bookkeeping Spreadsheet

> FREE Uber Logbook Spreadsheet

> FREE ABN & GST Registration

How To Claim an EV or Tesla on your Uber Taxes

Updated 28th of June 2024

Electric vehicles are the way of the future, and for Uber, rideshare and delivery drivers, they provide huge savings on running costs over traditional petrol cars.

But when it comes to working out your tax deduction for your EV on your Uber tax return, things get challenging.

In this article, I’ll explain everything you need to know about tax for EVs, including how much you can claim for the purchase of a Tesla or other electric vehicle for rideshare or delivery work, how to calculate your tax deduction for electricity when charging your EV at home, and the tax implications of installing a Tesla Wall Connector or EV home charger.

It’s important to note that the ATO have released some guidance for claiming electric vehicles, but there are still some gaps, especially when it comes to GST. So where the ATO haven’t provided specific guidance, the information in this article is based on interpretation of our existing tax laws. Given that EVs are quickly becoming mainstream, I’m sure we’ll see more from the ATO on this topic before too long, and when that happens I will update this article accordingly.

Note that DriveTax is an accounting firm specialising in tax for rideshare and delivery drivers, so this article is written with those drivers in mind. But this information applies equally to other ABN holders and small business owners too. There are some differences when claiming car use as an employee, so be sure to read that section toward the end of the article if it applies to you.

Quick Links

> Claiming The Purchase of an EV on Tax

> 2024 Financial Year – Depreciation for EVs and Teslas

> 2023 Financial Year – Temporary Full Expensing Write-off for EVs and Teslas

> The Car Cost Limit for EVs and Teslas

> Claiming EV Electricity with the CPKM Rate

> Claiming EV Public Charging

> Claiming GST on Charging an EV

> Claiming a Tesla Wall Connector or EV Home Charger

> Entering EV Expenses in the DriveTax Ultimate Uber Spreadsheet

> Claiming an EV as an Employee

General Rules for Claiming Electric Vehicle Tax Deductions

Before we dive into the specifics of claiming EVs on tax, let’s first recap a few basics of claiming car expenses for rideshare and delivery drivers.

Claiming The Logbook Method for EVs

If you want to claim a tax deduction for your EV’s electricity use and running costs, and claim a deduction for the purchase of your EV itself, you MUST have a valid logbook. Your logbook must go for 12 weeks, it must list all of your business trips (you don’t have to include private trips), and must include the odometer readings at the start and end of each business trip.

Once you’ve completed your logbook, you’ll be able to calculate your logbook percentage. You can then claim a tax deduction for this percentage of all of your car’s running costs, including electricity/fuel, insurance, rego, servicing, repairs and cleaning. For a more detailed explanation of claiming car expenses, visit our Complete Guide to Tax for Uber Drivers.

To answer a common question, if you’ve purchased your EV less than 12 weeks before 30 June that’s okay. As long as the first logbook entry is on or before 30 June, you can use it for that financial year. You’ll just need to wait until your 12 weeks is complete before you can lodge your tax return. To take this one step further, what if you pick up your car on 30 June, but don’t start Uber until July? That’s okay too, you can put a private use entry into your logbook on the 30th and that will count as the start of your logbook.

(Note that for previous years under the TFE rules, the write-off occurred on the date of the first business trip. So to be eligible to claim in a given year, you must have done at least one Uber trip before 30 June.)

If you have already kept a logbook within the last five years, as long as your pattern of usage is still roughly the same you can continue using that logbook percentage for your new car, no need to keep a new logbook. However, if your pattern of usage has changed significantly (we usually say +/- 10%) then your old logbook becomes invalid, and you must start a new one.

Visit this article on our blog for more detail about the ATO’s rules on Keeping A Logbook For Uber.

Claiming The Cents Per Kilometre Method for EVs

If you haven’t kept a valid logbook, then your only other option for claiming car expenses is to use the cents per km method. The ATO gives us a set rate that we can claim per km, up to a maximum of 5,000km per vehicle per year, which apply equally to EV’s:

- 2022-2023: rate of 78 cents per kilometre, which gives a maximum deduction of 78c x 5,000km = $3,900

- 2023-2024: rate of 85 cents per kilometre, which gives a maximum deduction of 85c x 5,000km = $4,250

- 2024-2025: rate of 88 cents per kilometre, which gives a maximum deduction of 88c x 5,000km = $4,440

At first glance, this might look like a decent tax deduction, considering that EVs are quite cheap to run and maintain. But you must also consider your claims for depreciation (including the Instant Asset Write Off) and loan interest, which are the two largest costs of owning an EV. You won’t be able to claim these expenses unless you have a valid 12-week logbook.

My advice is always to keep a logbook regardless of which method you plan to use. Then at tax time each year, you can calculate both methods and claim whichever one gets you the best result.

One quick thing to note if you’re using the cents per km method: if your state charges you an EV road user levy, this is covered in the cpkm deduction already. So if you’re using the cents per km method you can’t claim a separate tax deduction for EV levies.

Claiming GST for Electric Vehicles

If you’re a rideshare driver or GST-registered business, you can claim back the GST that you paid on any business expenses, including the purchase of the car itself (up to the Car Cost Limit, more below). You don’t necessarily have to have a logbook to claim GST, the ATO allows you to make a reasonable estimate of your business use percentage instead. Jump here for more on GST for Rideshare Drivers.

Claiming The Purchase of an EV on Tax

There are a bunch of tax rules to keep in mind when claiming the purchase of a car on your business. I cover them all in detail in our article on Buying A Car For Uber, so here I’ll focus on the points that are most relevant when buying a Tesla or EV for Uber, rideshare or delivery driving.

Claiming the Purchase Cost of your EV

2024 & 2025 Financial Year – Simplified Depreciation for Small Business

For vehicles purchased from 1 July 2023 onwards, most EV owners can no longer claim a write-off for their vehicle because the ATO the Temporary Full Expensing Write-Off has ended.

In its place, the government is bringing back the Instant Asset Write-Off, but only assets costing under $20,000 are eligible, which excludes virtually all EV’s in Australia. (*The $20,000 threshold for 2025 has not formally been passed into law yet. We’ll update here once it’s confirmed.)

Instead, the primary depreciation method for EV owners will be Simplified Depreciation for Small Businesses. This method allows you to claim 15% in the first year of ownership and 30% of the remaining balance in each year after that. Once the closing balance reaches $20,000, you’ll then be able to write-off the remaining balance in the following financial year.

Alternatively, the traditional depreciation method is also available, which is a 25% diminishing value deduction, apportioned for days in the year of purchase. But for most drivers, Small Business Depreciation will give the best long-term tax result.

2023 Financial Year – the Temporary Full Expensing Write-Off for Teslas and EVs

For vehicles purchased between the 6th of October 2020 and the 30th of June 2023, under the ATO’s Temporary Full Expensing rules, you can claim a tax deduction for the whole cost of your car in the year of purchase instead of claiming depreciation over a number of years.

Alternatively, you can claim traditional depreciation, which is a 25% diminishing value deduction, apportioned for days in the year of purchase.

Note that in order to be eligible to claim the TFE write-off in 2023, you must have completed at least one business trip during the financial year. So if you’re purchasing close to 30 June you’ll need to pay attention to your timing.

Another important point to note is that the TFE write-off isn’t actually beneficial in every case. If claiming Temporary Full Expensing for your car will push your overall taxable income below the tax-free threshold, then some portion of your tax deduction would be wasted. So for some drivers, it’s actually better to opt out of the TFE write-off, and claim traditional depreciation instead, which spreads your car claim over a number of financial years.

If you think this might apply to you, consider having DriveTax prepare your tax return. We’ll run an analysis of your car purchase and your overall tax circumstances to work out the optimum strategy for claiming your car and maximising your tax benefit.

There are a few other tricks and traps to look out for when buying an EV:

Car Cost Limit for Teslas and EVs

The ATO’s Car Cost Limit sets the maximum tax deduction you can claim on the purchase of any car. If your car purchase cost is more than the relevant limit, then you can only claim up to the limit, and the rest of your car purchase cost is not deductible. Note that if you are registered for GST then you must exclude the GST on your car purchase when calculating the limit. Here are the limits:

- 2022-2023: Car Cost Limit = $64,741 x your logbook %

- 2023-2024: Car Cost Limit = $68,108 x your logbook %

- 2024-2025: Car Cost Limit = $69,674 x your logbook %

If you’re GST-registered, note that your GST claim is also capped to 1/11th of the Car Cost Limit. So the maximum GST credit you can claim for your car purchase is as follows:

- 2022-2023: Car Cost Limit for GST = $5,885 x your logbook %

- 2023-2024: Car Cost Limit for GST = $6,191 x your logbook %

- 2024-2025: Car Cost Limit for GST = $6,334 x your logbook %

So as an example, let’s say you purchase a Tesla for $90,000 (incl $8,182 of GST) during the 2025 financial year, you have a logbook of 80%, and you’re registered for GST.

- On your BAS you’ll get a GST credit of $6,334 x 80% = $5,067

- On your tax return you’ll be able to claim depreciation on $69,674 x 80% = $55,739

Claiming a Tax Deduction for Tesla Enhanced Autopilot and Self-Driving Capability

One particular trap that Tesla owners need to look out for is claiming the cost of Tesla Enhanced Autopilot, Tesla Self Driving Capability, and other add-ons to your Tesla or other EV purchase.

Regardless of whether you add these options at the time of purchase or at a later point, they form part of the cost of the car (costs added at a later point are referred to as the ‘second element’ of the cost base).

This means that if you’ve already used up the Car Cost Limit (which is common due to the price of Teslas), you won’t get any further tax deduction for these add-on features, even if you purchase them in a separate transaction at a separate time, and even if it’s in a different financial year.

So for example, let’s say you purchased a Tesla in March for $80,000, which means you’ve already hit the Car Cost Limit. Then in July you decided to purchase Enhanced Autopilot for $6,000. Since your initial purchase of the car already used up the Car Cost Limit, you won’t be able to claim any further tax deductions or GST credits for the Enhanced Autopilot.

You can read more about these rules in the ATO’s Guide to Depreciating Assets.

Non-Commercial Loss Rules and the $20,000 Test

Many Uber drivers who purchase and claim a new car on tax end up making an overall taxable loss on their sole trader business. This was is especially true for years where the TFE write-off was available (the 2023 and earlier financial years).

If you do end up with a loss, the ATO’s ‘non-commercial loss rules’ determine what happens to your loss in your end of year tax return.

In the vast majority of cases you’ll be referring to the ‘assessable income test’, which looks like this:

- If your assessable income is over $20,000 (or pro-rata) you can claim your loss as a tax deduction against your employee and other taxable income

- If your assessable income is under $20,000 (or pro-rata) then your loss must be ‘carried forward’. You will only be allowed to claim that loss as a deduction against rideshare/delivery profits in future financial years

Your assessable income is your gross income from rideshare or delivery driving, before deducting any expenses (e.g. Uber fees). If you’re GST-registered then you must exclude GST. If you’re using the DriveTax Delivery spreadsheet it’s the total at the top of Column B of the expenses spreadsheet, or if you’re using the DriveTax Rideshare Spreadsheet it’s the total at the top of Column D.

If you only started driving part-way through the financial year you can pro-rata the $20k threshold. For example, if you started driving on the 1st of February, that’s five months of driving. So your threshold would be $20,000 / 12 months x 5 months of driving = $8,333. This is the income level you’ll need to hit if you want to claim your rideshare/delivery loss against your other taxable income. Note that you can factor in out-of-the-ordinary events into your pro-rata calculation, for example if you were sick, or if you went overseas for a few weeks.

If you think you’ll have a loss from your rideshare or delivery business, and you want to claim it but you’re not sure if you’ll hit your threshold, I recommend making a note in your diary for the start of June to run your calculations and see where your assessable income is sitting. That way, if it’s looking like you’ll be short of your threshold you’ll have time to squeeze in some extra driving and earn some extra income before 30 June.

Paying Tax When You Sell Your Car Or Stop Driving

One last thing to keep in mind when claiming depreciation, the Instant Asset Write-Off or the TFE write-off. When you eventually sell your car or stop using it for business purposes, you’ll be required to declare the sale price or market value, multiplied by your logbook percentage, as taxable income. This is called a ‘balancing adjustment’.

The balancing adjustment is calculated as being the difference between the depreciated value of the car in your tax return, and its actual sale price, or if you didn’t sell and just stopped driving, then its market value at the time it stopped being a business asset.

Balancing adjustments can be especially tough if you previously claimed a write-off for your car, meaning its depreciated value is now $0. They can also be tough if you sell the car for close to the same price you bought it, or you stop driving not long after you buy the car, whereby your car’s value hasn’t dropped by much. In these cases, you’ll essentially have to pay back nearly all the tax benefits you received from the write-off claim.

If you’re planning to continue Uber driving, and you’re trading in a previous car for a new car, the depreciation claim for your new car may soften the blow a little. But since the ATO have removed the TFE write-off from 2024 onwards, the deduction for your new car is unlikely to cover the balancing adjustment of the old car, so there will likely still be some tax to pay.

To help cover these costs, if you claim the write-off on a new car purchase, I always recommend putting aside some of the tax refund you receive from your write-off to help you cover the future tax bill when you sell or stop doing Uber.

As you can see, claiming a new EV on tax is far from simple. I always recommend that for the year you purchase your car, you should have DriveTax or another tax agent prepare your tax return. We can work out the optimum strategy based on your income and circumstances, and make sure you’ve squeezed the maximum tax benefit out of your new car purchase. Here’s more information about our Express Tax service.

For more detail on these tax rules, plus a bunch of other FAQ’s about buying a car for rideshare or delivery, jump over to our article on Buying A Car For Uber.

Claiming Tax Deductions for Charging Your EV

ATO Cents Per Km Rate for EV Electricity

IMPORTANT TAX TIP FOR EV OWNERS: In order to use the 4.2 cents per km method for calculating your charging costs, you MUST record your odometer reading every year at 30 June. Pop a note in your calendar now!

To simplify the electricity usage deduction for EV drivers, the ATO has introduced a set rate of 4.2 cents per km to cover EV electricity costs. This is great news for rideshare and delivery drivers because it means you don’t have to track your car’s power consumption or perform complicated calculations on your electricity bill.

To be eligible to use this method, your car must be a zero-emissions electric vehicle, which means hybrid vehicles are not eligible. You must also have actually paid for electricity at home. It’s okay if the bill is not in your name, but if your electricity is bundled into your rent and can’t be separately identified, or you don’t pay for electricity at all, then you cannot use this method. And finally, you must have kept a valid 12-week logbook.

To calculate your deduction, you must record your car’s odometer at 30 June each year. Taking a photo of your odometer is the easiest way, make sure it’s timestamped, and then save it in your tax records. This will allow you to calculate the total number of kilometres your car has travelled for the year (i.e. business kms + private kms).

I strongly recommend setting a reminder on your phone or in your diary for 30 June each year to make sure you remember. If you started or stopped driving partway through the financial year you’ll use your odometer at your start or stop date.

For the 2023 financial year, the ATO understands that these are new rules, and drivers were not aware back on 1 July 2022 that they needed to keep these records. So for 2023 only, the ATO will allow you to make a reasonable estimate of your car’s odometer reading. The best way to make this estimate is by looking for the nearest odometer record you have at that time. Your EV might have internal records of its daily odometer readings, or perhaps when you have your car serviced the mechanic will normally record your odometer on the paperwork.

Once you have worked out the total kms that your car travelled for the financial year, the 4.2 cpkm calculation looks like this:

- Total Kilometres x 4.2 Cents per KM = Total Electricity Cost

- Total Electricity Cost x Logbook % = Tax Deductible Amount

Note that there is no GST on this claim, so it is not relevant for your BAS’s, only for your tax return.

Let’s look at an example. An Uber driver records their odometer on 1 July 2023 as being 10,000, and on 30 June 2024 it shows 50,000. They have a logbook that shows 80% Uber use because they also use the car for family transport.

- 50,000 ending kms – 10,000 starting kms = 40,000 kms of total car travel for the year.

- 40,000 km x 4.2 cents per km = $1,680 total electricity cost for the year

- $1,680 x 80% business use logbook = $1,344 tax deduction for electricity expenses

Claiming for Public Charging

If you choose to use the 4.2 cpkm method, you cannot claim any other deductions for public vehicle charging costs because they’re already factored into the 4.2cpkm rate.

If you primarily charge at home, and only use public chargers occasionally then this is no problem, you’ll likely be better off using the 4.2 cents per km method.

On the other hand, if most of your charging is at paid public chargers, then you can choose instead to claim for your public charging costs x your logbook %, and claim nothing for your at-home charging. If you mostly use public chargers, my advice is to keep all your public charging receipts, and at the end of the financial year run both calculations, public charging vs the 4.2cpkm method, and see which one gets you the largest tax deduction.

Claiming 4.2cpkm AND Public Charging

There’s one exception to the requirement to choose between the above two methods of 4.2cpkm or claiming public charging.

If your car has the functionality to track how many kWh of electricity you charged at different locations, then you can claim both methods. Note that this functionality has to be built into the car itself, tracking via an app doesn’t count.

If you’re eligible for this method, here’s an example to demonstrate how the calculation would work:

- The car’s software reports that between 1 July and 30 June, 75% of the car’s kWh of charging were drawn from home, and 25% of kWh were drawn from public chargers.

- Based on the odometer records at 1 July and 30 June, the car did 10,000km for the year

- Public charging receipts came to $400

- The driver kept a 12-week logbook that shows 80% business use

- Their claim for charging would be as follows:

- + At home charging = total 10,000km x 75% of kms attributable to home charging = 7,500km x 4.2cpkm = $315

- + Public charging = $400

- = Total electricity deduction = $315 + $400 = $715 x 80% Uber logbook = $572

The Actual Cost Method

The ATO also provides an option to claim your home electricity cost via the ‘actual cost’ method, but it’s incredibly complex and time-consuming, and usually only gives a small deduction, so most drivers who choose the public charging method just ignore home charging. But you can find the details at the end of this article if you want to know more.

Claiming A Tax Deduction for an EV Home Charger

Many EV owners will choose to install a Tesla Wall Connector or EV home charger in order to charge their EV more efficiently.

From a tax perspective, there has been a great deal of confusion around whether home EV chargers can be claimed as a depreciable asset or not. In their recently published tax guidance, in my opinion, we have still not been given a clear concrete answer on whether chargers can be claimed or not, because they only speak about companies providing chargers for their staff, and they don’t acknowledge sole traders specifically. However, if we follow the logic behind the company/employee rules, it does now seem more likely that sole traders are permitted to claim a depreciation deduction as well. Please exercise caution when claiming these deductions in your tax return, and I will update this article if the ATO publishes clearer information.

If you have purchased a home EV charger, you will need to include it as a depreciable asset within your motor vehicle schedule in your tax return. This is complex, and is beyond what I’m able to explain here. So if this applies to you, my recommendation is to have your tax return prepared by DriveTax or another tax agent.

Claiming GST for Charging Your EV

How To Claim GST on EV Charging

While the ATO have provided this great new simplified rate for claiming tax deductions for your EV charging, this doesn’t help rideshare drivers when it comes to claiming GST.

The 4.2 cents per km method cannot be used for your BAS’s. The only way to claim EV charging on your BAS’s is to claim your actual costs.

This is fairly straightforward for paid public charging, you’ll just claim the GST on the amount you pay, just the same as paying for fuel or any other car expenses.

Where things get tricky is with charging your EV at home. Calculating your actual electricity cost is incredibly complex, it involves tracking the power consumption while your vehicle is charging, and then calculating your home’s electricity cost per kWh. I have included instructions for this process at the end of this blog post. But you may decide that it’s not worth the effort of all the tracking and calculations, especially if you have solar power and don’t pay much for electricity, you don’t drive a great deal, or your business use percentage is low. Many drivers choose to just not worry about claiming GST on their home charging, and just use the ATO’s 4.2 cpkm rate at the end of the year. The choice is yours!

For instructions on how to enter these expenses in your DriveTax spreadsheet, keep reading below.

Entering your EV Expenses in the DriveTax Ultimate Uber Spreadsheet

If you don’t get have a copy of the DriveTax Ultimate Uber Spreadsheet download the free version here, or learn more about the full version here.

If you’ve already got the free spreadsheet but need the latest update, do a search in your email inbox for DriveTax, you should find an email from us in the last week of June with links to the latest version.

If you’ve already purchased the full version of the spreadsheet or the online course, you’re entitled to lifetime free updates. Log into your DriveTax online portal anytime to download the latest copy.

The latest version of the DriveTax Ultimate Uber Spreadsheet is the 2024-2025 version, which was released at the end of June 2024.

We’ve fully updated the spreadsheet to cover all of the ATO’s permitted methods of claiming your EV charging, including the 4.2cpkm method. If you had both public charging and home charging expenses, the spreadsheet will calculate both options and use whichever one gets you the biggest tax deduction.

This spreadsheet is fully backwards compatible, so you can use it for previous financial years too.

If you’ve been using an earlier version of the spreadsheet, and you plan to lodge your own tax return on MyGov, we strongly recommend rolling your figures over to the latest version of the spreadsheet, to take advantage of the updated EV deduction calculations to maximise your claims. Feel free to email your existing spreadsheet through to us and we can roll it over for you.

If you plan on lodging your tax return through DriveTax then you don’t need to worry about which spreadsheet version you’re using. We’ll run all your calculations at our end as part of preparing your tax return to make sure you get the best possible result.

You’ll find step-by-step instructions on the Instructions tab of your spreadsheet for how to enter your charging expenses, so please be sure to read them carefully! If you have any questions about how to enter your EV expenses into your DriveTax spreadsheet please feel free to email us anytime!

Claiming EV Expenses as an Employee

If you also use your EV for employee work-related travel all of the same rules apply, except that the Small Business Depreciation/TFE write-off are not available. As an employee, you’ll instead claim traditional depreciation over a number of years using the diminishing value method at 25%.

Note that the Car Cost Limit that I mentioned does apply to employees as well. Also keep in mind that the rules around which trips are tax-deductible are different for employee travel vs business travel. This ATO page goes into more detail if you need it.

If you’re a rideshare or delivery driver and also use your car for tax-deductible employee travel, you’ll first need a 12-week logbook that shows your two separate percentages for business travel and employee travel. You’ll then make two separate claims in your tax return. In the business schedule, you’ll claim your business % of the cost of the car under the Small Business Depreciation rules or TFE write-off, and in the employee section (Item D1) you’ll claim the employee % of the cost of the car under traditional depreciation rules using the diminishing value method. So that’s two different types of depreciation, in two separate sections of your tax return, using your two logbook percentages. Not at all straightforward! If this applies to you, consider having your tax return prepared by a tax agent such as DriveTax.

What Next?

- If you need to register for an ABN or GST (or you just want to learn more about your tax obligations), use our free service as part of the DriveTax Free Uber Tax Info Pack

- Start a logbook if you don’t have one already. Read our blog post on Keeping A Logbook For Uber for more information

- For more detail on the various tricks and traps of claiming a new car on tax, read our article on Buying a Car for Uber

- See our BAS Services Page for help claiming back the GST on your car purchase

- See our Tax Returns Page to learn about having your tax return prepared by DriveTax

- If you’d like to learn more about buying a car for Uber, including how to calculate depreciation, and how to lodge your own BAS and tax return, check out our online course Understanding Uber Taxes.

Questions? Thoughts? Pop them in the comments below and I’ll get right back to you!

Safe driving! – Jess

About the Author – Jess Murray CPA – Uber Accountant

Jess Murray is a CPA Accountant and registered tax agent. She’s been working in personal and small business tax for 15 years, and has been specialising in tax for Australian Uber Drivers for the last 7 years as the Director of DriveTax. She also teaches an online course called Understanding Uber Taxes.

Jess is on a mission to make taxes straightforward and manageable for Uber drivers across Australia.

The information in this article is general in nature and does not take into account your personal circumstances. If you’d like to know how this article applies to you, please contact us to arrange a consultation, or talk to your accountant.

Other Posts You Might Like….

Bonus Content – How to Calculate Your Actual Electricity Costs

Now that the ATO has introduced the 4.2cpkm rate for claiming electricity, it’s no longer necessary for EV owners to track their charging or calculate their actual electricity costs from their utility bills. This is a great thing because the calculations required were truly a pain. The cpkm rate is a huge time-saver for all drivers.

Having said this, the actual cost method is still permitted by the ATO, and for a small number of drivers it may result in a larger deduction. So for completeness, I have included our actual cost calculation method from before the cpkm rate was introduced, just in case it’s useful for anyone.

How To Calculate Your EV Electricity Cost for Tax

Step 1 – Calculate Your Car’s Electricity Usage in kWh

The first piece of information you’ll need is how much electricity your car has used while charging.

For most EVs, the app that comes with your car will track your charging history and electricity usage. But it’s important that you’re able to see the location of your charges as well because for tax purposes you’ll need to know specifically which ones were at home. Check if your car’s app geo-tags your charges (it may be a feature you have to manually turn on), and if so, check whether it allows you to generate a weekly or monthly report of your charging history that you can filter by location, just to pick out the home charges.

If your car’s app can’t show you this data, you may like to consider a third-party app such as EEVEE. Otherwise you’ll need to keep manual notes of which charges were at home, perhaps by keeping a notepad next to your home charger.

Ultimately, what you’ll need to end up with is a total of your car’s electricity usage in kWh, specifically from at-home charging. I recommend totaling up this usage either weekly or monthly, depending on how often you sit down and do your bookkeeping, but best not to leave it longer than monthly.

Step 2 – Calculate Your Home’s Average Electricity Cost per kWh

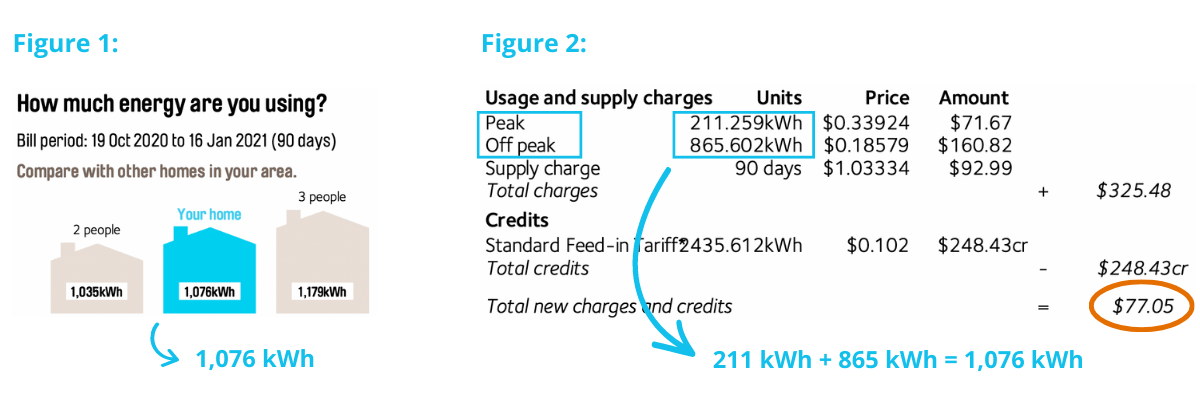

For this next step you’ll need to grab your latest electricity bill. You’re looking for the total electricity in kWh that your home used for the billing period. You might see this highlighted on the front page of your bill like in Figure 1 below, otherwise you might need to look for a table like in Figure 2, that shows your Peak and Off-Peak usage in kWh that you’ll manually add together.

We then apply this formula:

Total bill ($) / electricity usage (kWh) = cost per kWH ($/kWh)

In our example here, you can see the total electricity usage is 1,076kWh. It is shown in Figure 1 as a total, and also in Figure 2 by adding the highlighted Peak and Off-Peak usage figures together. We then take the bill total of $77.05 circled in orange and divide by the total electricity usage. So the final calculation is $77.05 / 1,076kWh = $0.0716 per kWh.

Regarding solar credits (the home in this example has solar panels that feed back into the grid), you’ll notice that we don’t need to do anything in particular in our calculation. That’s because we’re already factoring the credits in naturally by using the gross electricity usage against the net dollar cost of the bill. This method acts to apportion the solar credits across the usage per kWh, and so they are proportionately factored into our tax deduction. (Jump down a few paragraphs for more on the topic of solar).

The same is true for the daily supply charge, we’ve factored this into our calculation because we’ve used the total bill cost, which includes the supply charge. In other words, you are receiving a tax deduction for your car’s proportion of the daily supply charge as well as the electricity usage itself.

Once you’ve calculated your average cost per kWh, you’ll keep using this figure up until your next electricity bill arrives. Each time you receive a new electricity bill you should run a fresh set of calculations, and that’s the rate you’ll use on your weekly/monthly car electricity usage up until your next bill.

You’ll notice that there’s inherently a time lag factor here, because most people receive electricity bills every 2-3 months. So it’s unavoidable you’ll be using your electricity cost from up to three months ago against your current month’s car electricity usage. Unfortunately there’s nothing to be done about this, at least not without getting extremely complex in your calculations. This is where that ’reasonable’ balance of simplicity vs accuracy comes into play. As I’ve mentioned before the ATO understands these limitations, and it evens out over a period of time anyway, so it’s not a cause for concern.

Step 3 – Calculate Your Car’s Electricity Cost

From here it’s simple, just multiply your car’s electricity usage in kWh from Step 1 by your home’s average electricity cost per kWh in $ from your most recent bill in Step 2. This will give your car’s electricity cost for the period.

So following our example above, let’s say your car’s total electricity use for a month as per Step 1 was 1,000kWh, and your home’s average electricity cost as per Step 2 was $0.0716/kWh. So our Step 3 calculation is 1000kWh x $0.0716/kWh = $71.60 total electricity cost for the month.

The electricity cost is then treated just like any other car expense. If you’re GST-registered you’ll claim 1/11th of this ($6.51) x your logbook/business-use % on your BAS, and then the remaining cost (i.e. the GST-exclusive portion, being $65.09) x your logbook % as a deduction on your end-of-year tax return. Or, if you’re not GST-registered, then GST isn’t relevant, you’ll just claim the whole cost ($71.60) x your logbook % as a deduction on your end-of-year tax return.

If you’re using the DriveTax Ultimate Uber Spreadsheet, jump down below for instructions on how to enter your electricity cost in your spreadsheet

What About Using Solar Power?

Solar power adds another layer of complexity on top of an already complex calculation. It’s especially confusing if you charge your car during daytime hours from 100% solar power. This may you’re not incurring direct electricity costs, but of course there’s still an indirect cost, you’re using solar power that you would have otherwise put back into the grid or that would have charged your home battery.

The calculation method I described above does still work in this context. It allocates the dollars you actually spent on electricity bills against your car’s portion of the whole household power usage. So any reduction to your overall electricity bills thanks to solar power is also proportionately applied, thus ticking the ‘reasonable’ box.

There are of course calculation methods that are more precise than the method I detailed above. In theory you could track the specific cost of electricity on each separate occasion that you charge your car (on-peak, off-peak, solar/free), and find mathematical ways to account for electricity put back into the grid and so forth, and end up with a more exact end result. But as I mentioned before, given the level of data tracking and the complexity of calculations this would require, the ATO would not expect the average taxpayer to use such an extreme level of precision. You are free to be more precise if you wish, but the percentage method described above is absolutely adequate for solar-powered homes, or just use the 4.2cpkm rate.

The other quick solar-related tax question is of course the cost of installing solar panels or a house battery. No, these are not deductible, as they’re primarily a home improvement. You can claim costs relating to your car’s electricity usage in your home but not the cost of your home’s electrical system itself.

Hi Jess,

I have purchased an EV and started driving to Uber as of today previously I was using my old car for 6 months. Can you let me know how much would be my first-year depreciation if I don’t claim TFE?

Also given the factor the battery has only 8 years warranty how long will it take to zero down on car cost?

Also I have a capital loss of $7500 from last year tax return is this something I can claim driving Uber this year?

Thanks

Hi Narendra. I’m sorry I can’t give personalised tax advice here. You may like to check out the ATO’s depreciation calculator here. If you want to calculate traditional depreciation (i.e. no write-off), the easiest way is to choose Asset > Individual and on the next page choose Work Related Car Expenses, and effective life is 8 years with Diminishing Value. As you can see, with the DV method the depreciation goes on indefinitely but getting smaller each year, it never gets down to zero. To answer your other question, no, capital losses can only be claimed against capital gains, they can’t be claimed against business profits. – Jess

Hi Jess, I bought the Tesla EV and am doing an Uber driver part-time now. I have a full-time employee job, can I able to claim the tax reduction at end of the financial year from my employee income if I earn more than 20k from Uber? For the cost involves in buying the car expenses (lease), the question raised based on your below statement, Kindly clarify.

If your assessable income is over $20,000 (or pro-rata) you can claim your loss as a tax deduction against your employee and other taxable income

Hi Mark, yes, if your income is over $20k pro rata, you can claim a business loss as a tax deduction against your employee income. To explain the pro-rata rule, if you started driving on the 1st of March, that means you’re driving for 4 months out of the year, so your threshold is $20k x 4/12 = $6,666. If you’re registered for GST, don’t forget that it’s based on your GST-exclusive income. Our article on Buying A Car For Uber has more information that might be helpful. – Jess

Jess – just wondering if you’ve received a reply from the ATO regarding the private ruling request yet? Cheers.

Hi Josh, I’ve been notified that it’s not far away, so please keep checking back here and I should have an update for you soon. – Jess