FREE Uber Tax Info Pack

FREE 5-Day Email Course to learn the ATO’s Uber tax rules

FREE Uber Expense Spreadsheet so you never miss a deduction

FREE Uber Logbook Spreadsheet to claim your car expenses

FREE ABN & GST Registration (if you need it!)

FREE Uber Tax Info Pack

> FREE 5-Day ‘Uber Tax Essentials’ eCourse

> FREE Uber Bookkeeping Spreadsheet

> FREE Uber Logbook Spreadsheet

> FREE ABN & GST Registration

Uber GST Explained – The Complete Guide to GST for Uber Drivers

Updated 3rd of June 2023

Uber GST is one of the biggest learning curves for new rideshare drivers. Thanks to specific ATO GST laws for Uber drivers, we have to register for GST, lodge BAS’s, and pay additional taxes to the ATO, things that most Australian small businesses don’t have to worry about.

So my goal in this blog post is to make Uber GST as simple and stress-free as I can. I’ll explain the rules on whether you have to register for GST as an Uber driver, how GST on your rideshare income is calculated, and how to lodge your Uber BAS to the ATO.

Table of Contents

1) Introduction to GST for Uber Drivers

1.1) What Is GST?

1.2) Do Uber Drivers Have To Register for GST?

1.3) Why Do Uber Drivers Have To Register for GST?

1.4) How To Register for GST for Uber

1.5) Choosing your GST Registration Date

2) Calculating GST On Uber Income & Expenses

2.1) GST On Uber Fares & Fees

2.2) GST On Uber Expenses

2.3) Saving For Your GST Bill

3) BAS’s for Uber Drivers

3.1) What Is A BAS?

3.1) How Do You Lodge A BAS?

Skip To The Good Bits!

Looking for an accountant to lodge your BAS?

Jump here to read about DriveTax Express BAS service.

Looking for the DriveTax FREE Spreadsheet to help you lodge your own BAS?

Jump here for the free spreadsheet download.

Want to learn how to lodge your own Uber BAS on MyGov?

Jump here to read more about the Understanding Uber Taxes online course and MyGov BAS video tutorials.

Introduction to GST for Uber Drivers

First, let me explain exactly what GST is, and how it applies to Uber Drivers.

What Is GST?

GST stands for Goods and Services Tax. It’s a tax of 10% on all the goods and services sold in Australia. GST is everywhere.

We pay GST on our groceries, clothes, phone bills, haircuts and Netflix subscriptions. If you look at your tax invoice for almost any purchase you make you will see the GST. But as regular consumers we don’t really pay attention to GST, all that matters to us is the total price.

As GST-registered business owners, however, suddenly GST becomes very important. All GST-registered businesses in Australia must pay 1/11th of their business income to the ATO as GST. For Uber drivers, this means 1/11th of the Gross Fares, Split Fare Fees, Booking Fees, Tips, and all other amounts that you receive from each passenger.

You can then claim back GST credits for any GST you pay as part of your business related expenses. This includes the GST Uber charges you on their Service Fees, plus the GST on all the other parts of the fare you pass on to Uber, such as Split Fare Fees and Booking Fees. It also includes the GST on other Uber expenses such as fuel, mints, stationery, and your mobile phone bill (although some of these need to be apportioned for your Uber vs private use percentage).

GST-registered business pay their GST to the ATO quarterly on a Business Activity Statement, which is like a mini-tax return but just for GST. I’ll explain this in a little more details below.

Do Uber Drivers Have to Register For GST?

Yes, all Uber and Rideshare drivers must register for GST right from when they start driving for Uber

- Uber & Rideshare Drivers: ALL rideshare drivers must register for GST, because the ATO has special tax laws for taxi and rideshare drivers. The usual GST Registration threshold of $75,000 threshold does not apply, instead we must register for GST from the first dollar we earn.

- UberEats & Food Delivery Drivers: The ATO’s special rules only apply to ridesharing services, not food delivery. So if you only do food delivery, and you don’t do any rideshare driving, then you do not have to register for GST. The only exception to this rule is if your total ABN income, including any subcontracting or business income and of course food delivery, is more than $75,000. Assuming you’re under this threshold, the rest of this post doesn’t really apply to you, so to learn more about your ATO registration and tax rules head over to Tax for UberEats & Food Delivery Drivers.

- Rideshare AND Food Delivery Drivers: If you do both rideshare AND food delivery. then the rideshare rules apply. You must register for GST, and you must pay GST to the ATO on both your rideshare and your food delivery income.

Once you register for GST, that GST registration applies to ALL income you earn on your ABN. So, as mentioned before, if you drive for both Uber and UberEats, you will have to pay GST on both. Likewise, if you do freelance or subcontracting work or have other small business income on your ABN, that income will now be subject to GST as well.

> Register for GST for free with the DriveTax Free Uber Tax Info Pack.

A Quick History Lesson: Why Do Uber Drivers Have To Pay GST?

The ATO’s law forcing taxi drivers to register for GST has been around for decades. This rule was introduced because the government sets fixed taxi fares across Australia. This created an uneven playing field between big taxi companies earning more than $75,000 who had to pay GST on their income, versus the one-man owner-drivers who were under the $75,000 threshold and didn’t have to pay GST. So the government solved this unfair advantage by forcing all taxi drivers to register for GST no matter how much they earned.

Uber launched in Australia in 2012 and at first the ATO didn’t know what to do. At that time Uber was running through a foreign company, in some states Uber was illegal (although illegal income is still taxable!), and of course taxi drivers were angry and protesting against their new competition. But the biggest question for the ATO was whether rideshare income was taxable, and whether rideshare drivers were subject to the same rules as taxi drivers when it came to registering for GST. All of this made things very confusing for Uber drivers who were just trying to do the right thing.

In May 2015 the ATO announced they had analysed the tax law and found that an Uber was a taxi under the definition in our tax law, and therefore Uber drivers had to register for, and pay, GST. Uber appealed, and the final court battle happened in February 2017. During the appeal, the ATO’s legal team read out definitions of a taxi out of SIX different dictionaries. The dictionaries all stated that a taxi service is any service that drives passengers from A to B for money. The court concluded that while a yellow car with ‘TAXI’ on the side and a light on top is certainly a common form of taxi, it’s not the only possible kind that fits the definition. They found that Uber, and by extension all rideshare services, meet the dictionary definition too.

Fast forward to today, and the ATO’s rules on rideshare and GST are crystal clear and strictly enforced. The ATO make Uber send them the details of all Uber drivers, and anyone who isn’t registered for GST will receive a letter forcing them to comply with the tax rules.

How To Register for GST for Uber

Getting your Uber GST Registration is easy, and free. You can submit your own application on the ATO website, or you can use our FREE DriveTax ATO Registration service, which is part of our free Uber Tax Info Pack. It takes only a few minutes to fill your contact details and preferred start date into our online form, and then we’ll prepare and submit your ATO application within two business days.

Note that is it possible to register for GST monthly, but I don’t recommend it. If you’re planning to lodge your BAS’s through an accountant, lodging 12 BAS’s per year instead of 4 will triple your accounting fees. Or if you plan to lodge your own BAS’s, lodging monthly is three times as much work. Some Australian businesses also have to option to register annually, but this is not available for taxi or rideshare drivers.

To register for GST, you also need an ABN. An ABN is an Australian Business Number, and every Uber, rideshare and food delivery driver must have one. You only get one ABN for your lifetime and you must use that same ABN for all your business activities. So if you already have an ABN you must use that ABN for Uber too, or if you’ve had an ABN in the past that is now cancelled you must reactivate it.

If you’ve never had an ABN before we’ll get one for you at the same time we register you for GST. Or if you’ve had one before just fill it into our GST Registration form and we’ll add your GST registration to your existing ABN. Check out this post on our blog for more about ABN’s for Uber and UberEats

Choosing your GST Registration Date

You can only register for GST once you have started the application process for Uber or another rideshare company. If possible you should do this before you start spending money on startup costs such as vehicle checks, permits and other fees so that you can claim back any GST you paid on these expenses. The same is true if you plan to buy a car for Uber. By starting the Uber application process and registering for GST before you buy the car, you may be able to claim back the GST on buying your car for Uber.

Calculating GST On Uber Income & Expenses

The ATO calculation of GST on Uber fares and GST on Uber fees can be confusing. Instead of simplifying things and just asking rideshare drivers to pay GST on their net profits, the ATO want us to calculate things the long way around. But do rest assured, you will only pay GST (and income tax) on the profits that go into your pocket, and not on Uber’s money! Let me show you how it works.

GST On Uber Fares & Fees

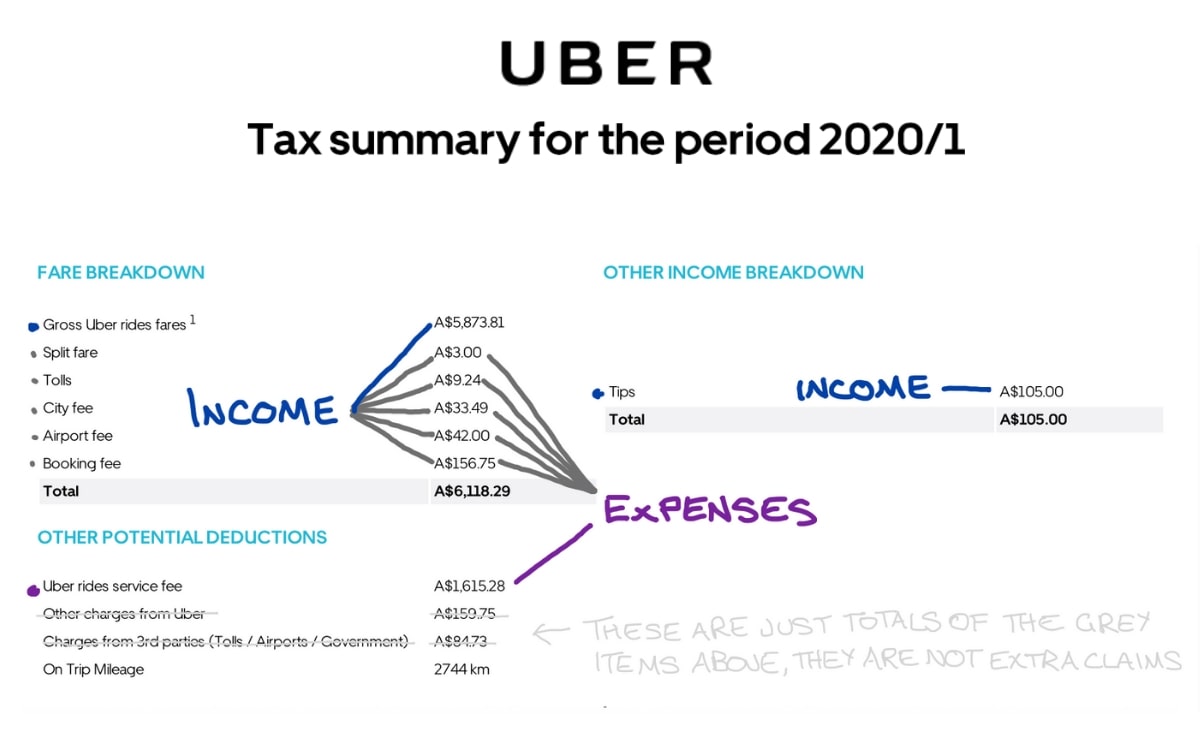

Any business in Australia that is GST-registered must give 1/11th of their sales to the ATO as GST. As an Uber or rideshare driver, this means that 1/11th of the Gross Fares plus 1/11th of all other amounts a rider pays for the ride (Booking Fees, Split Fare Fees, Airport Fees etc) must be passed on to the ATO. Then, as GST-registered business you can claim back GST credits for the GST (usually 1/11th) included in any expenses for your business. This includes the Uber Service Fees, all the extra fees you pay on to Uber (Booking Fees, Split Fare Fees, Airport Fees etc), plus car running costs, mobile phone bills, stationery and all other costs of being an Uber driver. Here’s an example of what this looks like on a monthly Uber Tax Summary:

So here’s how the tax calculation works in our example Uber figures above:

Grey Items: You receive these amounts from your rider as income, and then you pass them on to Uber as an expense. As you can see they cancel each other out, meaning you pay $0 GST on these amounts. And that makes sense, because it’s Uber’s money, not yours, so naturally you shouldn’t pay tax on it. But the ATO still requires you to show them as sales first and pay the GST, and then claim them as expenses and claim back that GST.

Income:

Gross Sales = Uber Fares + Split Fare Fees + Tolls + City Fees + Airport Fees + Booking Fees + Tips

GST on Sales = Gross Sales ÷ 11

Expenses:

Expenses = Uber Service Fees + Split Fare Fees + Tolls + City Fees + Airport Fees + Booking Fees

GST on Expenses = Expenses ÷ 11

GST Payable:

GST on Sales – GST on Expenses = Net GST Payable/Refundable

GST On Uber Expenses

In addition to your rideshare expenses that we covered above, here’s a list of other common GST claims for Uber drivers. The ones marked with (%) may need to be apportioned for business vs private use:

- Car Expenses (%)

- Fuel

- Insurance

- Repairs

- Servicing & Maintenance

- Tyres

- Cleaning

- Accessories

- Hire/Rental Fees

- Other Expenses

- Accountancy

- Computer Expenses

- Courses & Training

- First Aid Kit

- Internet (%)

- Mobile Phone (%)

- Music Subscriptions (%)

- Parking (only during an active shift)

- Rider Amenities (mints, tissues etc)

- Stationery

- Sunglasses

- Tolls

Expenses that are NOT claimable on your BAS:

- These expenses do not have GST so they cannot be claimed in your BAS. But they are still tax deductions so they can be claimed on your end of year income tax return.

- Bank Fees

- Car Depreciation

- Car Loan Interest

- Car Loan Repayments

- Car Registration

- Some Government Fees, Licences etc

- Water

- These expenses are either considered personal expenses or otherwise are not deductible

- Clothing

- Coffee

- Fines

- Food

- Parking at Home

- Personal Comfort

- Personal Hygiene

- Prescription Glasses (only sunglasses can be claimed)

You don’t need a formal 12-week logbook to claim car expenses on your BAS. Instead, for BAS purposes, the ATO only requires you to make a reasonable estimate of the percentage that you use your car for rideshare vs private/other use. But you do still need an official 12-week logbook for your end of year tax return, so my advice is that you might as well keep a proper logbook anyway. But in the meantime, if you haven’t started your logbook yet or you’re only partway through your 12 weeks, it’s nice to know you have the backup option to estimate your percentage for your rideshare BAS instead.

> To learn more about keeping a rideshare logbook, download our Free Tax Info Pack

Saving For Your GST Bill

It’s important to manage your GST obligations and save for you GST bill as you go. Otherwise you may get to BAS time and find yourself stuck with a GST bill you can’t pay.

The best way you can do this is by setting up a separate bank account especially for tax savings. Each time you get paid, transfer a set percentage of your earnings into the savings account.

It’s difficult to say exactly how much you should put aside because everyone’s expenses are different, which affects how much GST you’ll pay. But in our experience lodging BAS’s for thousands of drivers, most driver’s GST bills end up being somewhere between 5% and 8% of their net earnings. So if you’re someone who likes to play it safe, put aside 8% of what you receive in your bank account from your rideshare companies. Or alternatively if you want to save the minimum, then put aside 5% for now with the understanding that you may need to top up a little extra at BAS time.

Don’t forget that at the same time you’re saving for your GST bill you also need to be saving for your income tax bill. Visit our blog post on Saving for Your Uber Tax Bill to learn more about this.

BAS’s for Uber Drivers

I won’t go into too much detail here, because I’ve written a separate post specifically about BAS’s for Uber Drivers. If you want more detail about lodging your Uber BAS, due dates, and how to pay your GST bill, be sure to check it out. In the meantime, here are the basics.

> Learn more about Uber BAS’s with our Ultimate Guide to BAS for Uber Drivers

What Is A BAS?

A BAS (short for Business Activity Statement) is a form that GST-registered sole-traders and businesses must fill in and lodge to the ATO. On the form you’ll declare your sales and expenses, and calculate your GST bill payable to the ATO.

Most Uber drivers are registered for GST on a quarterly basis, which means they must lodge their BAS to the ATO each quarter. The quarterly dates are as follows:

- Quarter 1 – 1st July to 30th September

- Quarter 2 – 1st October to 31st December

- Quarter 3 – 1st January to 31st March

- Quarter 4 – 1st April to 30th June

How Do You Lodge A BAS?

There are three ways to lodge your Uber BAS to the ATO.

- Lodge yourself via a paper form

- Lodge yourself online on MyGov

- Lodge through a tax agent

If you plan to lodge your own Uber BAS, the DriveTax Uber Spreadsheet is essential. Easily enter your rideshare income and track your expenses, and then the spreadsheet does all of your GST and percentage calculations for you. At the end of the quarter the spreadsheet gives you the totals you need to enter into your Uber BAS, allowing you to lodge online in minutes.

> Download your Free Uber Spreadsheet as part of our Free Uber Tax Info Pack

If you’d like learn step-by-step how to lodge your own rideshare BAS, our Understanding Uber Taxes online course teaches you everything you need to know. It includes 30+ video lessons on Uber and rideshare tax, a detailed video tutorial on how to use the DriveTax Spreadsheet, and also a complete video tutorial on how to lodge your BAS on MyGov, plus lots more.

> Learn how to lodge your own Uber BAS step-by-step with the Understanding Uber Taxes online course.

Alternatively, if you’d like a tax agent to lodge your BAS for you, our DriveTax Express BAS service is your perfect choice. The Express BAS form gathers your Uber income and expenses, and then we process your BAS within two business days. If we have any questions or suggested extra deductions we’ll contact you by email to chat further. Then your completed BAS is lodged to the ATO, and a copy delivered to your inbox. All of this is great value at $99.

What sets DriveTax apart from other rideshare tax companies is that your BAS is completed directly by a CPA accountant right here in Australia. We don’t use offshore staff or AI automation. So you can be confident that a fully qualified accountant is preparing your rideshare BAS and individually checking that your expense claims are maximised to get you the best possible BAS.

> DriveTax Express BAS service for Uber and Rideshare drivers

In Summary

So in summary, here are your key steps in managing and lodging your taxes for Uber and rideshare:

- Get an ABN and register for GST Go >

- Track your expenses with the DriveTax Uber Spreadsheet Go >

- Put aside some of your Uber earnings each week to save for your tax and GST bills Go >

- Lodge your quarterly BAS’s via MyGov or through the DriveTax Express BAS Service Go >

- If you want to lodge your own BAS’s, check out the Understanding Uber Taxes online course for a full video tutorial Go >

Questions? Thoughts? Pop them in the comments below and I’ll get right back to you!

Safe driving! – Jess

About the Author – Jess Murray CPA – Uber Accountant

Jess Murray is a CPA Accountant and registered tax agent. She’s been working in personal and small business tax for 15 years, and has been specialising in tax for Australian Uber Drivers for the last 7 years as the Director of DriveTax. She also teaches an online course called Understanding Uber Taxes.

Jess is on a mission to make taxes straightforward and manageable for Uber drivers across Australia.

The information in this article is general in nature and does not take into account your personal circumstances. If you’d like to know how this article applies to you, please contact us to arrange a consultation, or talk to your accountant.

Hi Jess

Do the incentives paid to Uber drivers attract GST. I know this will be assessable income but is gst included in these figures,

Hi Angelika, yes all the amounts on your tax summary that you receive from Uber are subject to GST, including incentives and tips. If you’re using the DriveTax spreadsheet this will all be calculated for you. – Jess

Hi, I am not doing ride share, but delivery and other work.

I’ve projected that I’m on track to earn over $75,000 for this financial year if I continue earning at the rate I am – will I still need to register for GST?

Thanks!

Hi Derrick, yes, the overarching GST threshold still applies, you must register for GST if your sales are over $75,000. You will then need to declare ALL of your ABN income on your BAS, and you can claim GST on all of your expenses. – Jess

Hi, I was driving for uber eats from September to August 2023 and then registered for GST in October to driver rideshare. Will I need to pay GST for the uber eats income?

Hi Jai, you must pay GST on ALL types of income that you earned starting from the date of your GST registration. You do not have to pay GST on any income that you earned while you were not registered for GST. – Jess

Hi Jess,

I have found discrepancies between the toll charges provided in Uber’s monthly summary and the toll charges I see on Linkt. I’m just wondering should I enter the data provided by Uber in the “BAS income” and then input the actual deducted data by Linkt in the “expense”? However, it seems that the Excel sheet you provided has formulas locking the toll data in the “expense.” Any information would be greatly appreciated.

Hello, your Uber statements will only show tolls that were incurred while you have a passenger in the car. But the ATO allows you to claim tolls in between passengers as well. Please refer to the Instructions tab of your DriveTax spreadsheet, you’ll find instructions for how to capture your tolls between passengers. If you have any problems you can reach out via email. – Jess

Hi Jess, I am new to Uber and trying to set myself up for Tax time. I can’t find anything on your website to suggest how much of a percentage I should put away for Tax time? This is a second job for me. So won’t be doing any full time driving – it is just Uber Eats as well. Any information would be greatly appreciated.

Hi Tenille, this article on our website might be helpful: Saving for your GST and Tax Bills. – Jess

Hi I am Uber passenger driver , and I registered uber passenger

If I want to be didi or ola driver passenger do I need to register gst or only for uber is enough?

Hi Mohsen, you must register for GST if you do ANY Uber driving, it doesn’t make a difference which company. – Jess

Hi Jess,

I am confused between

Items to Calim for deduction for GST

Items to claim for deduction for ITO.

For example –

I bought the car for $33000 and paid $3000 GST Which I can claim over 4 or 5 years. So – ($3000/4)x 30% (assuming Uber % use) = 225 – GST deduction Claim

For Income tax deduction I can claim depreciation of the car over 4 or 5 years I can claim this as a deduction ex GST – So (30000/4) x 30% = 2250 – Income tax deduction,

Am I right here? If so, is the same for Insurance, Fuel, Uber Rego, Booked Hire Service License, Phone, Internet, Service or maintenance – all excluding GST?

Thanks

KP

Hi KP, let me direct you to our article on Buying A Car For Uber, I think it will answer your questions. – Jess

Hi Jess

Do we need to file GST quarterly or Annually?

Thank you

Hi Maaz, there is a specific rule for Uber drivers that they must register for GST quarterly, the annual option is not permitted. This is confirmed on the ATO website here. – Jess

This is all about booking fee. It makes me confused. I have seen negative(deduction) and positive(payment) in my weekly statement.

What is this all about. I know driver partners need to pay GST component to the ATO. What about the rest. Is it income or expense to the driver partner.

Hi Wilson, the Booking Fees are both a negative and positive, so they net out to zero. You can find the explanation under the heading Calculating GST On Uber Income & Expenses, and there is another explanation relating to taxable income here. – Jess

Hi Jess,

I did Uber Eats delivery for 8 months, changed to Uber driver for 1 week. I want go back to Uber eats again. Do I need to register GST? As my delivery income is under 30k.

Hi Ana, the ATO’s technical rule is that you must be registered for GST when you are doing rideshare. If you have decided you won’t do rideshare then you will need to call the ATO to deregister from the date you finished. You will still need to lodge a BAS and declare your income and expenses from that period. It’s obviously a pain to go to all that trouble for one week, but unfortunately that’s how the ATO’s rules are set – Jess

Hi Jess,

Recently I registered for GST planning to drive for Uber. As it took more than a month to get my driver accredition I started doing food delivery. Now, I changed my mind and want to do only food delivery and do not want to do ride share. Can I cancel my GST registration as I don’t want to drive rider share and my income in food delivery will not exceed $75K in a financial year? Please note I have not complete a single trip in ride share.

Hi Shravan, in order to cancel your GST registration, you must call the ATO directly on 13 28 66. The ATO have a specific rule for rideshare drivers where a GST cancellation can’t be done by a tax agent and can’t be done online, they want to speak to the rideshare driver directly before they will process the cancellation. You can explain your situation to the ATO, it’s possible that they’ll backdate the cancellation for you but I can’t be sure, you’ll have to chat to them and see. – Jess

Hi Jess, I’m a translator and provide services to a couple of companies on my ABN but I was not required to register for GST. Recently I started to drive uber and I have registered for GST. The question is that: Should I now pay GST on my payments from translating services?

Hi Kosta, that’s correct. Once you register for GST, you must be GST on ALL of your ABN income. – Jess

hi, I met with a accident can I deduct the insurance amount with gst

Hi Shareek, Yes you can claim a tax deduction for any insurance excess amounts you have to pay where the accident was directly connected to your Uber driving. If it happened while driving for personal reasons then you cannot claim. You must check the paperwork carefully to see how much GST was included in the payment because it may not be the usual 10% or it may even be $0. Ask your insurance company for a tax invoice if you are not sure. – Jess

I’ve had some passengers ask if they are paying GST and if so why is it not displayed on the receipt. They wish to claim these rides through work.

Hi Cath, good question. Technically, since the transaction for a ride is directly between you and the passenger, the responsibility for tax invoices rests with you. For trips under $82.50 you are not required to issue a tax invoice (ATO confirmation here), the receipt that the rider can download from the app is sufficient. For trips over $82.50 technically you are required to issue a tax invoice on request, and in theory you should carry an invoice book in your glovebox so that you can write one up if needed. In practice, I’m quite sure most drivers don’t do this.

Here’s a snippet from Uber’s webpage for corporate and business rider accounts, they essentially wash their hands of responsibility and say “we’ll put you in touch with the driver, it’s up to them”. This may seem slack on their behalf, but keep in mind they have no idea whether a driver is GST-registered or not, has changed their GST-registration etc, so I can understand why it’s not really legally possible create a tax invoice on the drivers behalf.

If you’re ever asked to create a tax invoice for a rider you can find the ATO requirements here. Handwritten on a piece of paper is fine, or if you’re requested by email afterwards just type it up in Word. – Jess

Hi Jess,

I would like to know that if I am register for GST and I pay this quarterly what happens if at the end of the financial year I do less that $au75.000 does the government give me the GST back??

Thanks

Hi Frederico, no the $75,000 threshold does not apply to rideshare drivers. If you earn more than $1 from rideshare driving you must register for GST. Then you will pay 1/11th of your income to the ATO as GST, and also claim back any GST that you pay on your expenses. This is a final tax, there are no refunds at the end of the year. The article above goes into more detail on exactly how this works. – Jess

What is the limit for not paying a taxi in Uber?

Hi Haidar, I think you’re asking about the GST threshold for Uber? The normal $75k GST threshold does not apply to Uber and taxi drivers, so you must register for GST from the first $1 you earn. You can find all the information in the blog post above. If you want to learn about paying income tax please visit our blog post on Income Tax for Uber Drivers. – Jess

Hi Jess,

I am a full-time employee and have a salary above 75k per year and the company I work for pays my taxes, I am planning to do Uber in my spare time. I wonder if my turnover from Uber becomes on top of my personal salary? Then in the GST form do I have to select the 75k – 149k option. Or are they considered separately?

Hi Tania, it only includes business turnover, not your employee income. So the answer to that question for almost every rideshare driver will be under $74,999. – Jess

Hi Jess,

Got another question here, when claiming GST on purchase for BAS, we can only claim our business percentage for petrol, car wash ect. For tax return can we use the cents per km method to claim our expense instead, which means the expense on BAS might not be the same as that on tax retrun. Thank you again!

Hi Lynn, yes it’s fine, and in many cases necessary, that the car claims for BAS and tax return don’t match. Anyone who does not have a logbook would be claiming their estimated percentage of car expenses on their BAS, and then the cents per km method on their tax return. – Jess

Appreciate your help, Jess!

Hi Jess, I know that Income Tax and GST are two different kinds of tax, and we must pay both. The question is when we claim deductions when preparing Tax Return, we can only claim the remaining amount (the total cost minus GST) as an income tax deduction, correct? if so, what about the income – can we exclude GST as well? Many thanks.

Hi Lynn, you’re exactly right, both income and expenses are declared excluding GST in your end of year tax return. To put it a different way, the GST (1/11th) is the tax office’s money, so you are never taxed on this, you are only taxed on your share (10/11ths). – Jess

Thanks so much for your quick response, enjoy the rest of your day!

Hi Jess,

I’m just wondering I have been driving for a year and i haven’t registered GST yet. If i register now, can I back date it? do I need to lodge 4 BAS in one go?

Hi Tim, yes you can (and must) backdate your GST registration to the date you started rideshare driving (or a tad earlier if you had expenses in getting set up and on the road). You will need to catch up on lodging all the BAS’s for that period. They don’t necessarily have to be lodged all on the same day, but you should try to lodge them as soon as possible. If you think it will take some time it’s best to give the ATO a call and let them know you are working on catching up and doing the right thing but that you need some extra time and usually they can make a note of this to help avoid any fines in the meantime. – Jess

Hi Jess, just wanting to know if we have to take into account any bonuses Uber has given to us in our quarterly bas or just at the end of the year….thank you regards vince

Hi Vince, normally yes, bonuses and rewards from Uber are subject to GST because they are connected to activities (i.e. driving) in Australia. The exception is where Uber pay a one-off special bonus to every driver in Australia – sometimes, depending on the reason for the bonus, this may be GST-free. But this has only ever happened once in Uber’s history in Australia so it’s quite rare. Most of the time they will be subject to GST and therefre must be included in your BAS. – Jess

In relation to GST, when making purchases i.e petrol, car wash, can you claim the full GST on the purchases?

Or would you only be entitled to claim the business percentage portion of the GST. This business percentage portion would be the percentage used from the logbook method.

If you chose the cents per KM method, how would you calculate the business portion of the GST on purchases?

Hi Antun, you can only claim your business percentage. For BAS’s you cannot use the cents per km method, that is only for tax returns. For your BAS if you don’t have to have a logbook, you can just estimate your business percentage. You can read more about BAS’s here. – Jess

Hi Jess,

Please advise I have earned Uber income less than 1K in financial year 2019-20 and paid GST as well. Do I need to mention Uber income when lodging income tax return for my primary job income.

I am very confused on this as I have already paid GST for uber income should I need mention uber income when lodging tax rerun, If I do so more tax will be deducted ?

Hi Shantnu, Income Tax and GST are two different kinds of tax, and you must pay both. You can read more about Income Tax here in our Uber Tax Guide – Jess

Hi Jess,

I have two questions.

First, in December 2019 I sold my old car for scrap ($300). I used this car occasionally for my full time job (around 1000km between July 2019 and December 2019), but I didn’t have a log book (last FY I claimed cents per km method). In February 2020 I bought a new car (financed) and in April 2020 I started driving for Uber (I have a log book since I started driving for Uber). Will I be able to use log book to claim car expenses for Uber and then using cents per km for my full time job (for my old car since I am not driving for work anymore due to COVID), or do I have to choose which method to use and stick with one for Uber and for my full time job?

Secondly, I have registered for GST after I purchased my new car and registered for Uber. Will I be able to backdate my GST registration in order to claim GST on purchase of the car?

Thank you

Hi Boris, you have to choose one method per car, so if you had two different cars during the year you can use two different methods if you want to. You can only backdate your GST registration if you have evidence that you started actively running your business at that earlier date. The most common way to do this is via your Uber Driver application process, so do a search in your inbox to see which date you started getting emails from Uber about that. – Jess

Hi, do all of you use an accountant to file your quarterly tax returns or file it yourself? How much does an accountant cost?

Hi Firos, thanks for commenting! Here’s a link to our BAS Services page. – Jess

Is there a deduction for Depn on my car allowed?

Hi Ramona, I recommend you check out our blog posts on Tax Deductions for Uber Drivers and also Buying a Car for Uber. – Jess

I’m doing Uber eats. Thinking about doing ride share. If I register for GST, is it correct I have no gst liability until I actually commence the ride share?

Hi Ramona, you don’t have to register for GST until the day you start driving for rideshare. You can register a little earlier if you want to claim the GST on your expenses, but you will have to pay GST on any income (including UberEats) so it’s up to you to decide whether it’s worthwhile. From the day you register for GST you will begin to pay GST on ALL income (including UberEats). – Jess

Thank you 😊

Hi jess,

I am applying to become a Uber eats food delivery driver, Do I still have to apply for GST and pay the ATO? I have read one part of your article stated that eats delivery with Uber no need GST applied. Is that true? if so, does that mean I pay the income tax only?

Hi Chillian, yes that is correct, you will find it in the second paragraph. UberEats drivers do not have to register for GST. I would not write it if it was not true! – Jess

If GST expenses are more than Income GST. Can we claim those ? If we claim in that case, do we get some benefit or we should put expenses equal to income ?

Hi Ashutosh, yes, if your GST on expenses is more that your GST on income for a given quarter then the ATO will send you a refund. – Jess

Dear Jess, Could you please let me know how I can calculate “GST turnover” for a month. Is that just the gross income minus GST for sale for the month? if so, what about the GST we pay for petrol etc. appreciate your thoughts

Hi Razi, GST turnover means the same as gross sales before deducting GST. You can find how to calculated this in the section above titled ‘Calculating GST On Uber Income & Expenses’. If this is in relation to caluclating your GST turnover for JobKeeper you may also like to check out our blog post on JobKeeper for Uber Drivers. – Jess

Hi Jess, Thumbs up for gr8 info in this article. I bought your paid spread sheet version as well. One thing Uber is charging 27.5% and we know 2.5% is GST. How to claim back/ include this 2.5% GST while filling out the spread sheet? Moreover, do Didi and Ola also keep a portion of GST (like Uber 2.5%) from drivers in their ride service fee, any idea? Many Thanks

Hi Max, first just to clarify. Uber and other rideshare companies do not take/keep any GST for you. They just charge you their fee and it includes GST exactly the same as your petrol and phone bill and other business expenses include GST too (take a look at your next fuel tax invoice to see what I mean, Uber’s fees are exactly the same!). Then you claim the GST on all those expenses back from the ATO. The DriveTax spreadsheet takes care of the GST calculation for you. So when you enter your Uber fees and all other expenses into the spreadsheet the GST is automatically worked out and the claim is added to your BAS. I hope that answers your question! – Jess